Pelaporan Surat Pemberitahuan (SPT) Tahunan Pajak Penghasilan (PPh) merupakan kewajiban bagi setiap wajib pajak. Namun dalam praktiknya, masih banyak wajib pajak yang mengalami kendala saat melaporkan SPT, salah satunya munculnya status lebih bayar padahal seharusnya nihil.

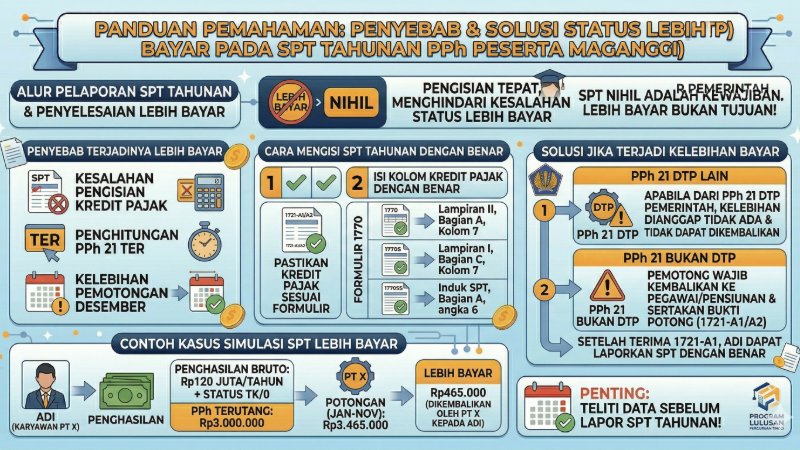

Penyebab terjadinya lebih bayar

Status lebih bayar dapat terjadi karena kesalahan dalam mengisi jumlah kredit pajak pada kolom PPh yang dipotong atau dipungut dalam SPT Tahunan. Kesalahan ini sering terjadi pada penghitungan PPh Pasal 21 yang menggunakan Tarif Efektif Rata-rata (TER), sehingga berpotensi menimbulkan kelebihan atau kekurangan pemotongan pajak pada bulan Desember.

Solusi jika terjadi kelebihan bayar

Apabila terjadi kelebihan pemotongan pajak, pemotong pajak wajib mengembalikan kelebihan pajak tersebut kepada pegawai atau pensiunan dan disertai dengan bukti potong formulir 1721-A1 atau 1721-A2. Namun apabila kelebihan tersebut berasal dari PPh Pasal 21 yang ditanggung oleh pemerintah, maka kelebihan pajak tersebut tidak perlu dikembalikan.

Cara mengisi SPT Tahunan dengan benar

Wajib pajak perlu memastikan bahwa jumlah PPh Pasal 21 yang dikreditkan dalam SPT sesuai dengan data pada formulir yang digunakan, yaitu:

Formulir 1770 diisi pada Lampiran II (1770-II) Bagian A Kolom 7.

Formulir 1770S diisi pada Lampiran I (1770S-I) Bagian C Kolom 7.

Formulir 1770SS diisi pada Induk SPT 1770SS Bagian A angka 6.

Contoh kasus SPT lebih bayar

Adi merupakan karyawan PT X dengan penghasilan bruto sebesar Rp120 juta per tahun dan status TK/0. Hingga bulan November, PT X telah memotong PPh Pasal 21 sebesar Rp3.465.000, sedangkan jumlah pajak terutang yang seharusnya dibayar hanya Rp3.000.000.

Dengan demikian terdapat kelebihan pemotongan pajak sebesar Rp465.000 yang harus dikembalikan oleh perusahaan kepada Adi. Setelah menerima bukti potong formulir 1721-A1, Adi dapat melaporkan SPT Tahunannya dengan benar sehingga dapat menghindari kesalahan status lebih bayar.

Kesimpulan

Pengisian SPT Tahunan perlu dilakukan secara teliti agar tidak terjadi kesalahan perhitungan yang dapat menyebabkan status lebih bayar. Wajib pajak disarankan untuk memeriksa kembali data yang dilaporkan sebelum melakukan pelaporan SPT.

Penyebab terjadinya lebih bayar

Status lebih bayar dapat terjadi karena kesalahan dalam mengisi jumlah kredit pajak pada kolom PPh yang dipotong atau dipungut dalam SPT Tahunan. Kesalahan ini sering terjadi pada penghitungan PPh Pasal 21 yang menggunakan Tarif Efektif Rata-rata (TER), sehingga berpotensi menimbulkan kelebihan atau kekurangan pemotongan pajak pada bulan Desember.

Solusi jika terjadi kelebihan bayar

Apabila terjadi kelebihan pemotongan pajak, pemotong pajak wajib mengembalikan kelebihan pajak tersebut kepada pegawai atau pensiunan dan disertai dengan bukti potong formulir 1721-A1 atau 1721-A2. Namun apabila kelebihan tersebut berasal dari PPh Pasal 21 yang ditanggung oleh pemerintah, maka kelebihan pajak tersebut tidak perlu dikembalikan.

Cara mengisi SPT Tahunan dengan benar

Wajib pajak perlu memastikan bahwa jumlah PPh Pasal 21 yang dikreditkan dalam SPT sesuai dengan data pada formulir yang digunakan, yaitu:

Formulir 1770 diisi pada Lampiran II (1770-II) Bagian A Kolom 7.

Formulir 1770S diisi pada Lampiran I (1770S-I) Bagian C Kolom 7.

Formulir 1770SS diisi pada Induk SPT 1770SS Bagian A angka 6.

Contoh kasus SPT lebih bayar

Adi merupakan karyawan PT X dengan penghasilan bruto sebesar Rp120 juta per tahun dan status TK/0. Hingga bulan November, PT X telah memotong PPh Pasal 21 sebesar Rp3.465.000, sedangkan jumlah pajak terutang yang seharusnya dibayar hanya Rp3.000.000.

Dengan demikian terdapat kelebihan pemotongan pajak sebesar Rp465.000 yang harus dikembalikan oleh perusahaan kepada Adi. Setelah menerima bukti potong formulir 1721-A1, Adi dapat melaporkan SPT Tahunannya dengan benar sehingga dapat menghindari kesalahan status lebih bayar.

Kesimpulan

Pengisian SPT Tahunan perlu dilakukan secara teliti agar tidak terjadi kesalahan perhitungan yang dapat menyebabkan status lebih bayar. Wajib pajak disarankan untuk memeriksa kembali data yang dilaporkan sebelum melakukan pelaporan SPT.

Submitting the Annual Income Tax Return (SPT) is an obligation for every taxpayer. However, many taxpayers still experience difficulties when reporting their tax returns, one of which is the appearance of an overpayment status even though the tax position should actually be nil.

Causes of overpayment

An overpayment status may occur due to errors in entering the amount of tax credit in the column for income tax that has been withheld or collected in the Annual Tax Return. This situation often occurs in the calculation of Income Tax Article 21 using the Average Effective Rate system, which can lead to either excess or insufficient tax withholding in December.

Solutions when an overpayment occurs

If an excess tax withholding occurs, the withholding agent is required to return the excess tax to the employee or pension recipient and provide a withholding tax certificate using form 1721-A1 or 1721-A2. However, if the excess originates from Income Tax Article 21 that is borne by the government, the excess tax does not need to be refunded.

How to properly complete the Annual Tax Return

Taxpayers need to ensure that the amount of Income Tax Article 21 credited in the Annual Tax Return matches the information shown in the relevant forms, as follows:

Form 1770 should be reported in Attachment II (1770-II) Part A Column 7.

Form 1770S should be reported in Attachment I (1770S-I) Part C Column 7.

Form 1770SS should be reported in the Main Form of 1770SS Part A number 6.

Example of an overpayment case

Adi is an employee of PT X with an annual gross income of Rp120 million and a tax status of single with no dependents. Until November, PT X had withheld Income Tax Article 21 amounting to Rp3,465,000, while the actual tax payable should only be Rp3,000,000.

This means there is an excess withholding of Rp465,000 that must be returned by the company to Adi. After receiving the withholding certificate form 1721-A1, Adi can report his Annual Tax Return correctly and avoid an incorrect overpayment status.

Conclusion

Completing the Annual Tax Return must be done carefully to avoid calculation errors that may result in an overpayment status. Taxpayers are advised to review their reported data carefully before submitting their tax returns.

Causes of overpayment

An overpayment status may occur due to errors in entering the amount of tax credit in the column for income tax that has been withheld or collected in the Annual Tax Return. This situation often occurs in the calculation of Income Tax Article 21 using the Average Effective Rate system, which can lead to either excess or insufficient tax withholding in December.

Solutions when an overpayment occurs

If an excess tax withholding occurs, the withholding agent is required to return the excess tax to the employee or pension recipient and provide a withholding tax certificate using form 1721-A1 or 1721-A2. However, if the excess originates from Income Tax Article 21 that is borne by the government, the excess tax does not need to be refunded.

How to properly complete the Annual Tax Return

Taxpayers need to ensure that the amount of Income Tax Article 21 credited in the Annual Tax Return matches the information shown in the relevant forms, as follows:

Form 1770 should be reported in Attachment II (1770-II) Part A Column 7.

Form 1770S should be reported in Attachment I (1770S-I) Part C Column 7.

Form 1770SS should be reported in the Main Form of 1770SS Part A number 6.

Example of an overpayment case

Adi is an employee of PT X with an annual gross income of Rp120 million and a tax status of single with no dependents. Until November, PT X had withheld Income Tax Article 21 amounting to Rp3,465,000, while the actual tax payable should only be Rp3,000,000.

This means there is an excess withholding of Rp465,000 that must be returned by the company to Adi. After receiving the withholding certificate form 1721-A1, Adi can report his Annual Tax Return correctly and avoid an incorrect overpayment status.

Conclusion

Completing the Annual Tax Return must be done carefully to avoid calculation errors that may result in an overpayment status. Taxpayers are advised to review their reported data carefully before submitting their tax returns.