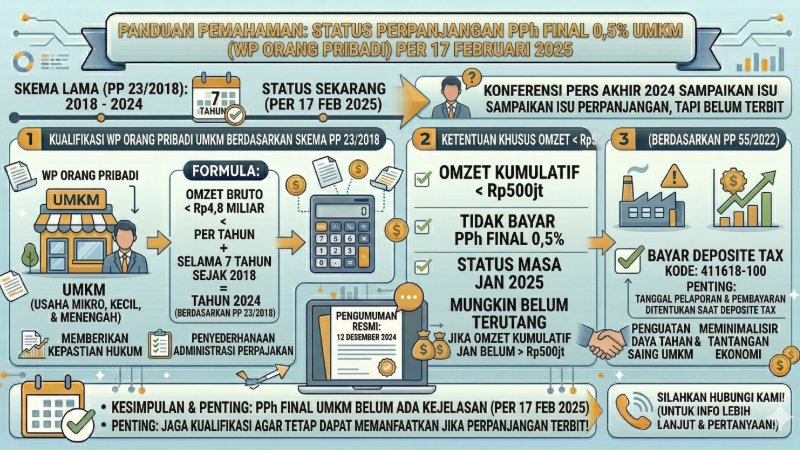

PPh Final 0,5% dari omzet bagi WP Pribadi UMKM, jadi diperpanjang di 2025?

UMKM dengan omzet kurang dari Rp 4,8M dapat menggunakan skema PPh final dengan tarif 0,5% dari omzet tiap bulan dan berdasarkan PP 55/2022 bagi yang omzet kurang dari Rp 500jt tidak bayar PPhnya. Skema PPh Final UMKM bagi WP Pribadi UMKM dapat digunakan selama 7 tahun sejak tahun 2018 (PP 23/2028) sehingga tahun 2024 merupakan tahun terakhir aturan ini berlaku.

Dalam konferensi pers terkait paket kebijakan diakhir tahun 2024 disampaikan akan isu perpanjangan jangka waktu PPh Final UMKM ini. Namun sampai dengan februari 2025, aturan dan teknis pelaksanaannya belum diterbitkan. Sehingga hari ini tanggal 17 februari 2025, WP Pribadi UMKM ini apakah masih diperkenankan menggunakan skema PPh final 0,5% dari omzet belum ada kejelasan.

Apabila WP Pribadi UMKM ini belum mencapat omzet Rp 500jt, PPh final tidak perlu dibayarkan, sehingga mungkin PPh Final masa Januari 2025 belum terutang. Namun jika sudah lebih dari Rp 500jt bagaimana?, Solusi yang dapat digunakan adalah dengan membayar deposite tax dengan kode 411618-100 untuk pembayaran masa januari 2025. Karena tanggal pelaporan dan pembayaran ditentukan saat tanggal deposite tax tersebut

UMKM dengan omzet kurang dari Rp 4,8M dapat menggunakan skema PPh final dengan tarif 0,5% dari omzet tiap bulan dan berdasarkan PP 55/2022 bagi yang omzet kurang dari Rp 500jt tidak bayar PPhnya. Skema PPh Final UMKM bagi WP Pribadi UMKM dapat digunakan selama 7 tahun sejak tahun 2018 (PP 23/2028) sehingga tahun 2024 merupakan tahun terakhir aturan ini berlaku.

Dalam konferensi pers terkait paket kebijakan diakhir tahun 2024 disampaikan akan isu perpanjangan jangka waktu PPh Final UMKM ini. Namun sampai dengan februari 2025, aturan dan teknis pelaksanaannya belum diterbitkan. Sehingga hari ini tanggal 17 februari 2025, WP Pribadi UMKM ini apakah masih diperkenankan menggunakan skema PPh final 0,5% dari omzet belum ada kejelasan.

Apabila WP Pribadi UMKM ini belum mencapat omzet Rp 500jt, PPh final tidak perlu dibayarkan, sehingga mungkin PPh Final masa Januari 2025 belum terutang. Namun jika sudah lebih dari Rp 500jt bagaimana?, Solusi yang dapat digunakan adalah dengan membayar deposite tax dengan kode 411618-100 untuk pembayaran masa januari 2025. Karena tanggal pelaporan dan pembayaran ditentukan saat tanggal deposite tax tersebut

Is the 0.5% Final Income Tax (PPh Final) on turnover for individual MSME taxpayers extended in 2025?

Micro, Small, and Medium Enterprises (MSMEs) with annual turnover of less than Rp4.8 billion may apply the final income tax scheme with a rate of 0.5% of monthly turnover. Based on Government Regulation No. 55 of 2022, MSME individual taxpayers whose turnover is below Rp500 million are not required to pay the final income tax.

The Final Income Tax scheme for MSME individual taxpayers can be used for a period of 7 years starting from 2018, as regulated in Government Regulation No. 23 of 2018. This means that 2024 is the final year in which this scheme formally applies for individual MSME taxpayers.

During a press conference regarding the government’s policy package at the end of 2024, there was discussion about the possibility of extending the MSME Final Income Tax period. However, as of February 2025, the official regulation and technical implementation guidelines have not yet been issued. Therefore, as of February 17, 2025, there is still no clear confirmation whether individual MSME taxpayers are still allowed to use the 0.5% final tax scheme based on turnover.

If the turnover of an individual MSME taxpayer has not yet reached Rp500 million, the final income tax does not need to be paid, meaning that the January 2025 tax period may not generate a tax liability. However, if the turnover has exceeded Rp500 million, a possible solution is to make a deposit tax payment using tax code 411618-100 for the January 2025 tax period. The reporting and payment date will follow the date when the deposit tax payment is made.

Micro, Small, and Medium Enterprises (MSMEs) with annual turnover of less than Rp4.8 billion may apply the final income tax scheme with a rate of 0.5% of monthly turnover. Based on Government Regulation No. 55 of 2022, MSME individual taxpayers whose turnover is below Rp500 million are not required to pay the final income tax.

The Final Income Tax scheme for MSME individual taxpayers can be used for a period of 7 years starting from 2018, as regulated in Government Regulation No. 23 of 2018. This means that 2024 is the final year in which this scheme formally applies for individual MSME taxpayers.

During a press conference regarding the government’s policy package at the end of 2024, there was discussion about the possibility of extending the MSME Final Income Tax period. However, as of February 2025, the official regulation and technical implementation guidelines have not yet been issued. Therefore, as of February 17, 2025, there is still no clear confirmation whether individual MSME taxpayers are still allowed to use the 0.5% final tax scheme based on turnover.

If the turnover of an individual MSME taxpayer has not yet reached Rp500 million, the final income tax does not need to be paid, meaning that the January 2025 tax period may not generate a tax liability. However, if the turnover has exceeded Rp500 million, a possible solution is to make a deposit tax payment using tax code 411618-100 for the January 2025 tax period. The reporting and payment date will follow the date when the deposit tax payment is made.